After one of the most explosive rallies in modern market history, few investors expect gold to pull off a repeat in 2026. But many top money managers are still betting on further gains, arguing that the forces that propelled bullion to a record remain in place. Gold surged 65% in 2025 — its strongest performance …

After one of the most explosive rallies in modern market history, few investors expect gold to pull off a repeat in 2026. But many top money managers are still betting on further gains, arguing that the forces that propelled bullion to a record remain in place.

Gold surged 65% in 2025 — its strongest performance in nearly half a century — as retail and institutional investors piled in alongside central banks.

In a year where almost every tailwind supporting the precious metal collided, from falling interest rates to geopolitical tensions, bullion even pushed through an inflation-adjusted high that had held since 1980.

Bloomberg spoke with more than a dozen money managers, whose firms collectively handle trillions of dollars of assets, to gauge sentiment after the historic year. Most of them said they’ve opted not to take too much money off the table, holding conviction in the metal’s longer-term appeal.

“We continue to expect gold to rally in 2026, as the drivers of its strong run remain intact,” said Ian Samson, a portfolio manager at Fidelity International. Samson trimmed his position during a frenzied stretch of October but has since added back, citing central bank buying, declining interest rates and high fiscal deficits as supportive factors.

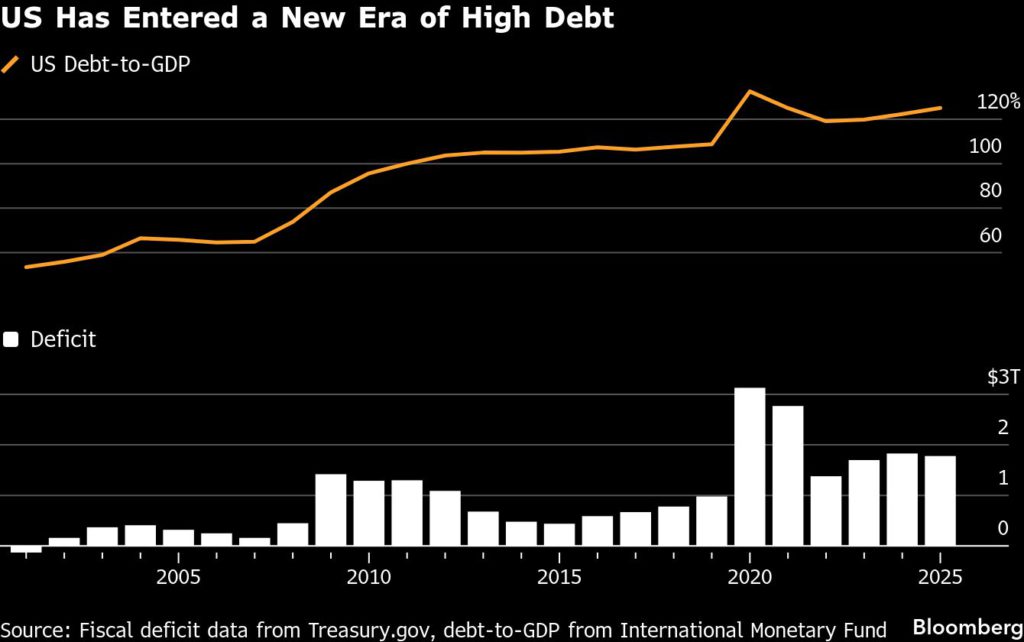

Investors also pointed to waning confidence in major developed-market currencies — driven by attacks on central bank independence and rising sovereign debts — as a key pillar of support for bullion. Swelling public debt in advanced economies fueled political discord through last year, from a congressional standoff in the US and paralysis in France to scrutiny of a record budget under Japan’s new leadership.

Gold is “basically an anti-fiat currency play now more than anything else,” said Mike Wilson, chief investment officer and strategist for Morgan Stanley. That view gained traction in the latter months of 2025, as the so-called debasement trade took hold and investors from Ken Griffin to Ray Dalio pointed to gold’s rise as a warning signal.

Wilson advises allocating 20% of one’s portfolio into real assets, including gold, as a hedge against inflation, replacing the traditional 60/40 stocks and bonds mix with a 60/20/20 split. He noted that the debasement story has gone mainstream.

“When everybody understands the story, you have to ask yourself: Well, is it priced now?” Wilson said. “I don’t think it’s fully priced, only because I don’t see the change in behavior yet. I don’t see the fiscal discipline anywhere in the world. In fact, I see the opposite.”

Darwei Kung, head of commodities and a portfolio manager at DWS Group, said his firm is holding a slightly larger-than-usual allocation to gold-related investments and expects to maintain that stance into 2026.

Kung sees the metal’s price increasing modestly by the end of the year. But he also expects short-term trading opportunities as gold is buffeted by broader market forces.

Pension and insurance funds showed increasing interest in gold through 2025, with some that had never held the asset before taking positions of around 5% of their strategic asset allocation, said Massimiliano Castelli, head of global sovereign markets strategy at UBS Asset Management. They were drawn by strong returns and gold’s potential to hedge against downside elsewhere in their portfolio, he added.

“Of course, we don’t see the same upside potential of last year, when gold was basically the best asset class of all,” said Castelli. “But we are still bullish on gold.”

History offers a note of caution. Outsized rallies have often been trailed by long stretches of lackluster performance. Bullion hit a record $1,921 an ounce in 2011, driven by fallout from the global financial crisis, but it took another nine years to return to that level. A prolonged bear market also followed gold’s record 127% surge in 1979.

Even so, gold remains lightly owned by US investors. Despite the record rally, gold exchange-traded funds account for just 0.17% of private US financial portfolios, according to a December Goldman Sachs Group Inc. analysis — six basis points below the 2012 peak. The bank estimates that each bout of buying that increases gold’s share of US portfolios by 0.01% would lift prices by about 1.4%.

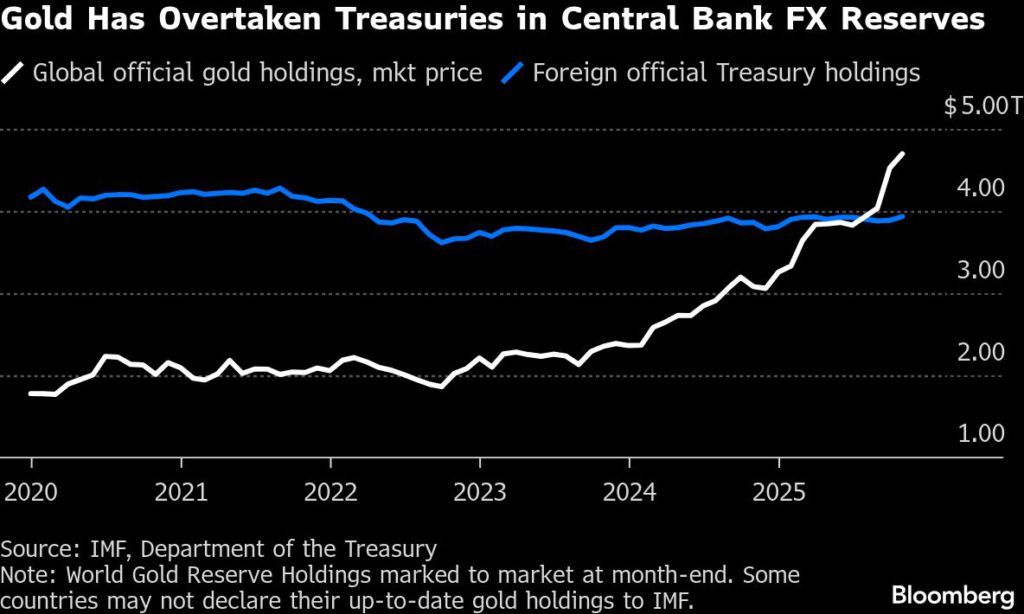

Continued central bank buying is expected to remain the most significant driver of further price gains, with Goldman Sachs expecting purchases of about 80 tons a month in 2026.

The pace of buying jumped in 2022, after the immobilization of Russia’s foreign-exchange reserves underscored the appeal of bullion, which cannot be frozen.

By Yvonne Yue Li, Jack Ryan and Yihui Xie